It is unbelievable how many times I've heard people telling me "the US has become self-sufficient in oil production," a group that includes some respectable members of the EU parliament. This is probably due to the confusion that the media have made on the fact that the US production has recently surpassed the US imports of oil. It is true, but that tells you nothing of how much oil the US still imports. And that is, actually, much more than it was at the time of the oil crisis and domestic consumption is on the increase (as you see in the figure above, from Art Berman's blog)

This misperception on the actual dependence of the US on imports is probably one of the reasons that led to the recent lifting of the ban on US exports, that dated from the time of the great oil crisis of the 1970s

Art Berman clarifies the situation and wonders why "consumption has increased by one-third and imports have doubled but we no longer need to think strategically about oil supply because production is a little higher?" Here is an excerpt from his post.

____________________________________________

The Crude Oil Export Ban–What, Me Worry About Peak Oil?

by Art BermanPosted in The Petroleum Truth Report on December 27, 2015

Congress ended the U.S. crude oil export ban last week. There is apparently no longer a strategic reason to conserve oil because shale production has made American great again. At least, that’s narrative that reality-averse politicians and their bases prefer.

The 1975 Energy Policy and Conservation Act (EPCA) that banned crude oil export was the closest thing to an energy policy that the United States has ever had. The law was passed after the price of oil increased in one month (January 1974) from $21 to $51 per barrel (2015 dollars) because of the Arab Oil Embargo.

The EPCA not only banned the export of crude oil but also established the Strategic Petroleum Reserve. Both measures were intended to keep more oil at home in order to make the U.S. less dependent on imported oil. A 55 mile-per-hour national speed limit was established to force conservation, and the International Energy Agency (IEA) was founded to better monitor and predict global oil supply and demand trends.

Above all, the export ban acknowledged that declining domestic supply and increased imports had made the country vulnerable to economic disruption. Its repeal last week suggests that there is no longer any risk associated with dependence on foreign oil.

What, Me Worry?

The tight oil revolution has returned U.S. crude oil production almost to its 1970 peak of 10 million barrels per day (mmbpd) and imports have been falling for the last decade (Figure 1).

Figure 1. U.S. crude oil production, net imports and consumption. Source: EIA and Labyrinth Consulting Services, Inc. (Click image to enlarge)

The tight oil revolution has returned U.S. crude oil production almost to its 1970 peak of 10 million barrels per day (mmbpd) and imports have been falling for the last decade (Figure 1).

Figure 1. U.S. crude oil production, net imports and consumption. Source: EIA and Labyrinth Consulting Services, Inc. (Click image to enlarge)

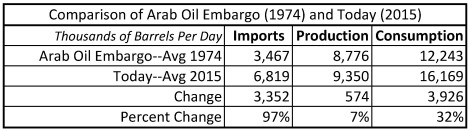

But today, the U.S. imports twice as much oil (97%) as in 1974! In 2015, the U.S. imported 6.8 mmbpd of crude oil (net) compared to only 3.5 mmbpd at the time of the Arab Oil Embargo (Table 1).

Table 1. Comparison of U.S. crude oil imports, production and consumption for 1974 (Arab Oil Embargo) and 2015 (Today). Source: EIA and Labyrinth Consulting Services, Inc.

(Click image to enlarge)

Production of crude oil is higher today by 7% but consumption has grown to more than 16 mmbpd, an increase of 32%. At the time of the Arab Oil Embargo, consumption was only 12 mmbpd.

So, consumption has increased by one-third and imports have doubled but we no longer need to think strategically about oil supply because production is a little higher?

We are far more economically vulnerable and dependent on foreign oil today than we were when crude oil export was banned 40 years ago.

What, me worry?

Continue reading on Art Berman's blog